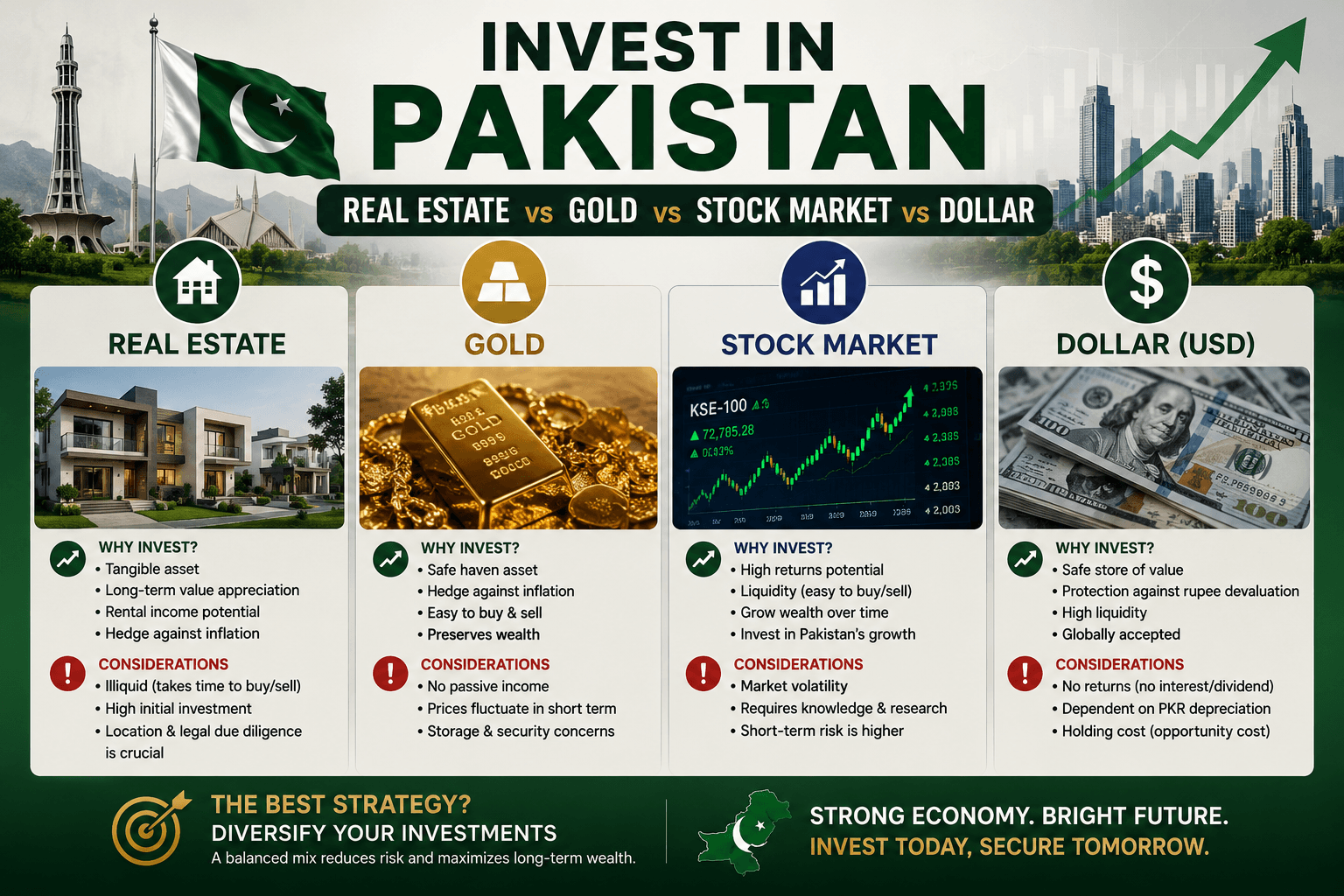

Investment in Pakistan

If you ask ten Pakistanis where to invest their savings, you will likely get ten different answers. Your uncle insists that gold is the only safe haven. Your colleague swears by DHA plots. Your banker recommends keeping dollars under the mattress. And that one friend who is always glued to his phone insists the KSE-100 is the only answer.

The truth is, Pakistan’s economic landscape over the last decade has been anything but ordinary. Between political upheavals, currency crises, IMF bailouts, a global pandemic, raging inflation, and interest rate shocks, every asset class has been tested to its limits. Some soared. Some quietly held their ground. Some disappointed.

So let us settle this debate once and for all with real numbers, real data, and real context. We put Pakistan’s four most popular investment options — Real Estate, Gold, the Stock Market (KSE-100), and the US Dollar — head to head across a full decade, from 2014 to 2024. The results may surprise you.

Read More: How to Invest wisely in Pakistan Stock market

Setting the Stage: Pakistan’s Economic Decade (2014–2024)

Before diving into the numbers, it’s important to understand the economic environment these assets had to survive and grow in:

- Inflation averaged between 8–12% annually for most of the decade, spiking to over 38% in 2023 — one of the highest inflation rates in the world at that time.

- The Pakistani Rupee (PKR) depreciated massively, falling from around Rs. 101 per US dollar in 2014 to over Rs. 280 per dollar by 2024 — a devaluation of more than 175%.

- Interest rates swung dramatically, from single digits to a historic high of 22% in 2023.

- Political instability caused repeated market shocks, from the PTI government’s ouster in 2022 to ongoing civil-military tensions.

- The real estate sector experienced a construction boom, a crackdown from FATF, a recovery, and another slowdown — all within one decade.

- The KSE-100 saw spectacular bull runs in 2016–2017, a painful bear market in 2018–2019, and then a stunning historic rally in 2023–2024.

For all the investments you need a good earning job. Read more about the best paying jobs in Pakistan

Gold — The Perennial Champion

Performance Summary

Gold has been Pakistan’s most culturally embedded investment for generations. From bridal jewellery to savings hoarded in almirahs, gold is part of the national psyche.

And the numbers do not disappoint.

| Year | Gold Price (PKR per Tola, 24K) |

|---|---|

| 2014 | ~Rs. 47,000 |

| 2015 | ~Rs. 47,450 |

| 2016 | ~Rs. 49,800 |

| 2017 | ~Rs. 73,200 |

| 2018 | ~Rs. 90,000 |

| 2019 | ~Rs. 1,30,000 |

| 2020 | ~Rs. 1,60,000 |

| 2021 | ~Rs. 1,25,000 |

| 2022 | ~Rs. 1,55,000 |

| 2023 | ~Rs. 2,50,000 |

| 2024 | ~Rs. 2,80,000 |

Source: Historical Pakistani Gold Market Data

10-Year Return: Approximately +495%

If you invested Rs. 1,00,000 in gold in 2014 (roughly 2.1 tolas), by 2024, that same gold would be worth approximately Rs. 5,95,000.

Why Did Gold Do So Well?

Gold’s phenomenal performance in Pakistan is driven by two forces acting simultaneously:

1. Global gold price appreciation: The international price of gold in USD rose significantly over the decade, driven by economic uncertainty, COVID-19, geopolitical tensions (Russia-Ukraine war), and central bank buying worldwide.

2. Rupee devaluation amplifier: This is the key Pakistan-specific factor. Because gold is priced globally in US dollars, every time the PKR weakened against the dollar, gold prices in rupees shot up even further. The rupee’s collapse from Rs. 101 per dollar to Rs. 280 per dollar effectively supercharged gold returns for Pakistani investors holding physical gold.

Risks of Gold Investment in Pakistan

- No income generation — gold does not pay rent or dividends

- Storage and security risks (theft, locker fees)

- Making charges on jewellery reduce effective returns

- Price can be volatile in short to medium term (gold actually dipped in 2021)

- Illiquid in large quantities — selling significant amounts can be complicated

Real Estate — The Favourite Son

Performance Summary

Real estate has long been Pakistan’s most beloved investment. The phrase “zameen kabhi maati nahi hoti” (land never turns to dust) captures the sentiment perfectly. But how has it actually performed?

Real estate returns in Pakistan are highly location-specific, so we use two representative benchmarks:

Prime Residential (DHA, Bahria Town, major city centres):

- Estimated average annual appreciation: 15–18%

- 10-year cumulative return: approximately +300% to +425%

Mid-tier Residential and Plots:

- Estimated average annual appreciation: 10–12%

- 10-year cumulative return: approximately +159% to +210%

| Scenario | Rs. 10 Lakh Invested in 2014 | Value in 2024 |

|---|---|---|

| Prime Real Estate (18% CAGR) | Rs. 10,00,000 | ~Rs. 52,00,000 |

| Prime Real Estate (15% CAGR) | Rs. 10,00,000 | ~Rs. 40,00,000 |

| Mid-Tier Property (12% CAGR) | Rs. 10,00,000 | ~Rs. 31,00,000 |

| Mid-Tier Property (10% CAGR) | Rs. 10,00,000 | ~Rs. 26,00,000 |

Figures are approximate and represent capital appreciation only; rental income would add further returns

The Real Estate Advantage: Rental Yield

What makes real estate different from the other three contenders is rental income — a steady, recurring cash flow. A well-located residential or commercial property in Lahore, Karachi, or Islamabad can generate a rental yield of 4–8% per year on top of capital appreciation.

This additional income stream, when reinvested, can push the effective 10-year return of real estate well beyond its raw appreciation figure.

What Drove Real Estate Prices in Pakistan?

- Rapid urbanisation and population growth creating housing demand

- Low-cost housing schemes and construction packages from successive governments

- Overseas Pakistani remittances fuelling property purchases (Pakistan receives among the highest remittances globally)

- Inflation of construction costs (cement, steel, labour), pushing up the value of existing properties

- Limited supply in prime, established locations (DHA, Gulberg, Clifton, F-6, F-7)

The Dark Period: 2022–2023 Slowdown

Real estate did not escape unscathed from Pakistan’s 2022–2023 economic crisis. Skyrocketing interest rates (22%), an IMF programme with tough conditions, and political instability caused a significant market slowdown. Transaction volumes dropped sharply. New bookings dried up. Many developers faced cash flow crises.

This is important context: real estate’s long-term average looks attractive, but the journey included real pain points.

Risks of Real Estate Investment in Pakistan

- Highly illiquid — you cannot sell a plot in an emergency the way you sell gold or stocks

- Large minimum investment required (barrier to entry)

- Legal risks: fraud, forged documents, disputed titles, housing society scams

- Maintenance costs, property taxes, and vacancies erode returns

- Regulatory uncertainty — government crackdowns on undocumented real estate deals

- Returns vary wildly by location; poor location choices can result in losses

US Dollar — The Safe Harbour

Performance Summary

Keeping money in US dollars has historically been a defensive strategy in Pakistan — a hedge against rupee devaluation rather than a growth investment. But the scale of the rupee’s collapse over the past decade turned this defensive play into a surprisingly strong performer. You can also invest in Dollars in Pakistan with easy steps.

| Year | USD/PKR Rate (Approximate) |

|---|---|

| 2014 | Rs. 101.55 |

| 2015 | Rs. 102.74 |

| 2016 | Rs. 104.71 |

| 2017 | Rs. 105.29 |

| 2018 | Rs. 121.57 |

| 2019 | Rs. 150.20 |

| 2020 | Rs. 161.00 |

| 2021 | Rs. 162.00 |

| 2022 | Rs. 176.00 |

| 2023 | Rs. 283.12 |

| 2024 | Rs. 278–280 |

Source: Link Exchange, State Bank of Pakistan, Wise Historical Data

10-Year Return: Approximately +175% (in PKR terms)

If you had converted Rs. 1,00,000 into approximately $985 in 2014 at the rate of Rs. 101.55/USD, and simply held those dollars, by 2024 at Rs. 280/USD, those same dollars would be worth approximately Rs. 2,75,800 — a gain of nearly 176%.

The Dollar’s Appeal

- Universally accepted store of value

- Protects against local inflation and political shocks

- Easily accessible (bank accounts, exchange companies)

- Liquid and portable

Why Dollars Fell Short of Gold

While dollars protected your purchasing power in international terms, gold went further because it too benefited from the same dollar-to-rupee currency shift — and additionally gained from the global rise in gold’s USD price. A dollar simply preserved its PKR value through devaluation; gold both preserved it and grew in USD terms simultaneously.

Important Caveat: Dollar Holding in Pakistan

Keeping large amounts of dollars in Pakistan is not without complications. Regulations around foreign currency accounts, restrictions on cash holdings, and the risk of government-imposed currency controls (as seen in various periods) add uncertainty. The open market rate and the official rate have historically diverged, creating arbitrage risks and regulatory exposure.

KSE-100 — The Volatile Rocket

Performance Summary

The Pakistan Stock Exchange‘s KSE-100 index is the most volatile of the four contenders. It has produced some of the most dramatic gains and losses in the region, making it the highest-risk, highest-reward option on this list.

| Period | KSE-100 Level (Approximate) |

|---|---|

| January 2014 | ~26,000 points |

| 2017 (Peak) | ~52,876 points |

| 2019 (Trough) | ~29,000 points |

| January 2024 | ~62,000 points |

| September 2024 | ~81,000 points |

| Early 2026 | ~189,000 points |

10-Year Return (Jan 2014 – Jan 2024): Approximately +138% to +212%

Note: Returns vary significantly depending on exact entry and exit dates, and this figure is capital appreciation only; dividend yield of 5–7% per year adds substantially to total returns.

The KSE-100 Roller Coaster

The stock market’s decade can be divided into distinct chapters:

2014–2017: The Bull Run The KSE-100 doubled in this period, making it one of Asia’s best-performing markets. Pakistan was classified as an Emerging Market by MSCI in 2017, attracting foreign institutional investment and fuelling euphoria.

2017–2019: The Great Crash What goes up must come down. A balance of payments crisis, IMF bailout talks, a new PTI government with uncertain economic policy, and an aggressive interest rate hiking cycle by the State Bank crashed the market from its 52,876 peak to below 30,000. Investors who entered at the top were devastated.

2020: COVID Shock — Then Unexpected Recovery The COVID-19 pandemic caused a brief but sharp crash in March 2020. The SBP’s emergency rate cuts and fiscal stimulus sparked a surprisingly fast recovery.

2021–2022: Political Turmoil Government changes, PTI’s ouster, and then the economic crisis created sustained uncertainty. The market struggled.

2023–2024: Historic Bull Run Pakistan entered an IMF programme, inflation peaked and started falling, interest rates began to come down, and the stock market exploded upward. The KSE-100 crossed 80,000 in 2024 for the first time in history, then continued its extraordinary rally past 189,000 by early 2026 — making it one of the best-performing markets globally in nominal terms.

Total Return Picture (Including Dividends)

When dividends are included — which averaged 5–7% per year across the KSE-100 — the total return picture improves significantly. A disciplined investor who stayed invested through the entire decade, reinvesting dividends, would have done considerably better than the raw index gain suggests.

Who Should Invest in Stocks?

The stock market rewards patience, research, and emotional discipline above all. The investor who panic-sold in 2019 or 2022 locked in devastating losses. The investor who held on — or better, bought more during crashes — was eventually rewarded. Timing matters enormously, far more than in real estate or gold.

Risks of KSE-100 Investment

- Extreme volatility — 30-40% drawdowns are common

- Political sensitivity — Pakistan’s markets react sharply to governance news

- Requires financial literacy and market knowledge

- Emotional discipline is difficult for most retail investors

- Liquidity is a double-edged sword (easy to sell panic at the wrong moment)

The 10-Year Scorecard: Head to Head

Assuming a starting investment of Rs. 10,00,000 in January 2014:

| Investment | Approx. Value by End-2024 | Total Return | CAGR (Approx.) |

|---|---|---|---|

| Gold | ~Rs. 59,00,000 | +490% | ~19.5% |

| Prime Real Estate | ~Rs. 40,00,000–52,00,000 | +300–420% | ~15–18% |

| US Dollar (held) | ~Rs. 27,50,000 | +175% | ~10.6% |

| KSE-100 (capital only) | ~Rs. 23,80,000–31,20,000 | +138–212% | ~9–12% |

| KSE-100 (with dividends) | ~Rs. 35,00,000–45,00,000 | +250–350% | ~13–16% |

| Inflation (CPI) | Purchasing power ~halved | ~-50% | — |

All figures are approximate estimates based on available market data and representative averages. Actual results will vary based on timing, location, and specific assets chosen.

Beyond Raw Returns: The Full Picture

Numbers alone do not tell the whole story. Here is how the four investments compare across other critical dimensions:

Liquidity: Access to Your Money in a Crisis

| Asset | Liquidity |

|---|---|

| Gold | High — physical gold can be sold the same day |

| Stocks | Very High — sell within minutes on PSX |

| US Dollar | High — exchange companies available nationwide |

| Real Estate | Low — can take weeks to months to sell; distressed sales require heavy discounting |

Accessibility: Minimum Investment Required

| Asset | Minimum Entry |

|---|---|

| Gold | Very Low — even a fraction of a gram |

| Stocks | Very Low — Rs. 5,000 can buy shares |

| US Dollar | Very Low — any denomination |

| Real Estate | Very High — typically Rs. 50 lakh to several crore for meaningful exposure |

Passive Income Potential

| Asset | Income Generation |

|---|---|

| Real Estate | Excellent — rental yield 4–8% per year |

| Stocks | Good — dividend yield 5–7% per year (KSE-100 companies) |

| Gold | None |

| US Dollar | None (unless in a foreign currency savings account) |

Protection Against Inflation

All four assets have historically outpaced inflation in Pakistan over the long run. However, gold has been the most reliable inflation hedge, followed closely by prime real estate. The rupee’s collapse means that holding cash (even savings accounts) has consistently destroyed purchasing power — which is why Pakistanis have been right to distrust simply keeping money in bank accounts.

Regional Nuances: Not All Real Estate Is Equal

A critical warning: real estate’s performance varies enormously by location and housing society. The headline returns in DHA Karachi, DHA Lahore, or Islamabad’s F-Sectors are vastly different from suburban schemes or newly developing areas.

Several housing societies across Pakistan have delivered near-zero or even negative real returns after accounting for legal disputes, delayed development, or poor location. On the other hand, well-located commercial property in established city centres has generated extraordinary wealth.

The lesson: Real estate’s average 300–400% gain over 10 years hides extreme variation. Due diligence, legal verification, and location selection are everything.

The Verdict: Which Investment Won?

Gold — The 10-Year Champion

By raw return, gold wins the decade comfortably. A combination of global price appreciation and massive rupee devaluation produced returns of nearly 5x on the initial investment. Gold also wins on accessibility, liquidity, and simplicity — anyone can buy it, store it, and sell it without legal paperwork.

Prime Real Estate — The Wealth Builder

Prime real estate in Pakistan’s major city developments delivered returns comparable to gold, with the added bonus of rental income. For those with the capital and patience, a well-chosen property in Karachi, Lahore, or Islamabad has been a spectacular wealth-building tool. However, the illiquidity, high entry price, and legal risks mean it is not suitable for all investors.

KSE-100 (With Dividends) — The Underappreciated Competitor

A fully disciplined investor who held the KSE-100 through its gut-wrenching crashes — reinvesting dividends along the way — would have done extremely well. The total return story (capital + dividends) brings stocks very close to real estate over the full decade. The problem is that very few retail investors actually managed to do this.

US Dollar — The Protector, Not the Winner

Dollars performed the important function of preserving wealth in the face of rupee collapse. They did not create new wealth — but they prevented its destruction. For those with foreign obligations, overseas family, or a need for internationally recognised value, holding dollars remains rational. As a pure wealth-creation tool in PKR terms, however, the dollar underperformed all three alternatives.

The Investment Wisdom for Pakistani Investors in 2025 and Beyond

Here is what a decade of data tells us:

1. Never hold idle cash in Pakistani rupees for the long term. Inflation and devaluation will erode your purchasing power mercilessly.

2. Gold remains the most accessible and reliable store of value for the average Pakistani. It requires no expertise, no legal paperwork, and no minimum investment.

3. Real estate rewards those with capital, patience, and research. Do not buy blindly. Verify legal status, check development timelines, and choose location above all else.

4. Stocks reward the brave and the disciplined. If you can hold through 30–40% crashes without panic-selling, the long-term rewards are substantial. Begin with blue-chip stocks or index-tracking mutual funds rather than speculative shares.

5. Diversification is not just a textbook concept. Spreading investments across gold, stocks, and — when possible — real estate, would have protected against any single asset’s bad years while capturing the upside of the good ones.

6. Rupee devaluation is a constant threat. Any investment that hedges against currency depreciation — gold, dollar, or assets whose prices track inflation — deserves a place in every Pakistani portfolio.

A Note on Insurance as a Financial Foundation

While this article focuses on investment returns, it is important to acknowledge what most Pakistani investors overlook entirely: financial protection through insurance.

A single medical emergency, accident, or loss of income can wipe out years of investment gains overnight. Before optimising for the highest returns, every investor — whether holding gold, property, or stocks — needs a financial safety net.

At Pakcover.com, we believe that insurance is not a cost; it is the foundation that allows you to invest with confidence. Protecting your life, health, property, and income ensures that a market crash, a fire, or a health crisis does not undo the patient, long-term wealth you have worked to build.

Conclusion

Pakistan’s investment landscape over the past decade has been a story of extraordinary opportunity and extraordinary risk, often existing side by side.

Gold, with its ~490% return, is the decade’s mathematical winner. Prime real estate, with its 300–420% appreciation plus rental yield, is arguably the most complete long-term wealth builder for those who could access it. Stocks, volatile and misunderstood, have rewarded disciplined, long-term investors far more than their reputation suggests. And dollars, while not the best performer in PKR terms, have served as an important wealth preserver in a country where the currency has lost more than 60% of its purchasing power.

The question is not which single investment “won” — the question is which combination is right for your circumstances, your risk tolerance, your liquidity needs, and your time horizon.

One thing is certain: in Pakistan’s economic environment, doing nothing and leaving money in a savings account is the only guaranteed way to fall behind.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice. Past performance of any asset class does not guarantee future results. Investment decisions should be made in consultation with a qualified financial advisor based on your individual circumstances.

All figures are approximations based on publicly available market data and industry reports. Actual returns will vary based on timing, location, specific asset selection, and transaction costs.

{kind=link}